What is the distribution of dividends among partners?

Index of contents

When a person invests in a corporation, he/she expects to make a profit. The mechanism used by these entities to distribute the profit among partners or shareholders is the distribution of dividends. In this post we tell you what requirements must be met and how and when the distribution is made.

The distribution of dividends is the act by which the profit obtained by a commercial company is distributed among the partners or shareholders of the company. The amount of dividends that each partner or shareholder receives will depend on the participation that he/she has in the capital stock.

Deadlines and requirements for dividend distributions

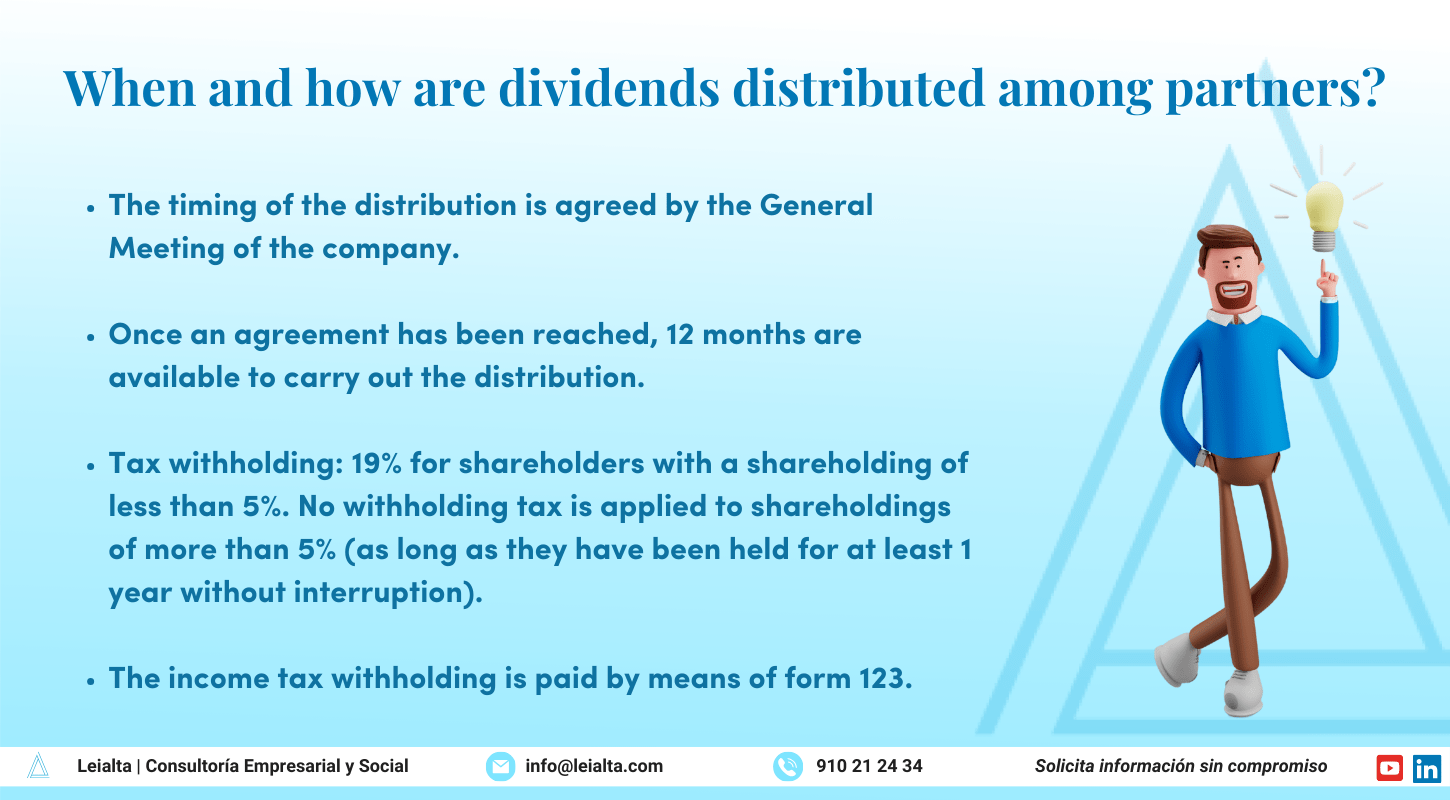

The moment for the distribution of dividends is agreed by the General Meeting of the company where the annual accounts of the previous year are approved. The minutes of this meeting will establish the form and the period in which the dividends will be distributed. The maximum period for the distribution of dividends is twelve months from the date of the distribution resolution. If this period is not complied with, the shareholder who has voted in favor of the distribution has the right of separation, but a series of legal requirements must be complied with.

The requirements for the distribution of dividends are as follows:

- The distribution resolution must be adopted at the General Meeting, which will establish the form and time of payment.

- The distribution will be made according to the shareholding in the capital stock.

- Priority will be given to those cases in which minimum dividends and dividends relating to directors’ remuneration have been established.

- The legal reserve must be covered, as well as the statutory reserves.

- Prior to the distribution of dividends it is necessary to cover losses from previous years.

- The shareholders’ equity cannot be less than the capital stock, either before or after the distribution.

In the previous case, we are talking about the distribution of dividends charged to the profit for the year, but there may be a distribution of dividends charged to reserves or on account of future profits. In the latter case, in addition to the resolution of the Shareholders’ Meeting, there must be an accounting report proving that there is sufficient liquidity to distribute dividends.

Percentages of withholding in the distribution of dividends

When dividends are distributed, a withholding tax must be paid to the tax authorities. If the shareholder is an individual or a legal entity with a shareholding of less than 5%, the withholding percentage is 19%. If the shareholding is higher than 5%, no withholding is applied, as long as the shareholding has been maintained throughout the previous year in an uninterrupted manner.

Procedure for withholding tax payment by means of form 123

Form 123 is used to pay the withholding to the tax authorities. The deadline for filing depends on whether a monthly declaration is filed: in this case it must be filed during the first 20 calendar days of the month following the month in which the dividend distribution has taken place.

If quarterly declarations are made, the form must be filed during the first 20 days of the months of April, July, October and January, in relation to the quarter prior to each month.

Form 123 is filed by means of electronic certificate or Cl@ve PIN and has the following content:

- Personal data of the declarant.

- Year and quarter being declared.

- Settlement. This section includes the withholding and income bases and the total amount of withholdings.

- Complementary. It is only used when a complementary declaration must be made to a previous one, which must be specified.

Once the tax return has been filed, the Treasury will proceed to charge the income (if the result of the liquidation is to be paid) by debiting the bank account indicated by the taxpayer on the 20th day of the months of filing mentioned above.

Is it possible to distribute dividends having debts with the Tax Authorities?

The distribution of dividends, if there are debts with the Tax Authorities, is possible as long as a guarantee of compliance with the outstanding tax obligations is provided. Therefore, if a company has debts with the Tax Authorities and decides to make a dividend distribution, it must notify the Tax Authorities and guarantee the debt before making the distribution. This also applies in the case in which a deferral or fractionation of payment of the tax debt has been requested.

In short, it is always advisable to have the help of a business consultancy specialized in commercial law and taxation of commercial companies, to study the case, optimize the taxes and carry out all the procedures to settle the corresponding taxes in due time and form. In addition, we can always offer more exclusive information for each case, for example, on the exemption of dividends for group companies.