Did you know that you can start operating with your business in Spain in only a few weeks? You don’t need to create a commercial company, you just need to obtain a non-resident NIF (Tax Identification Number). In this post we will tell you what steps to follow in order to get it.

Did you know that you can start operating with your business in Spain in only a few weeks? You don’t need to create a commercial company, you just need to obtain a non-resident NIF (Tax Identification Number). In this post we will tell you what steps to follow in order to get it.Which forms must be submitted in order to apply for a non-resident NIF?

Index of contents

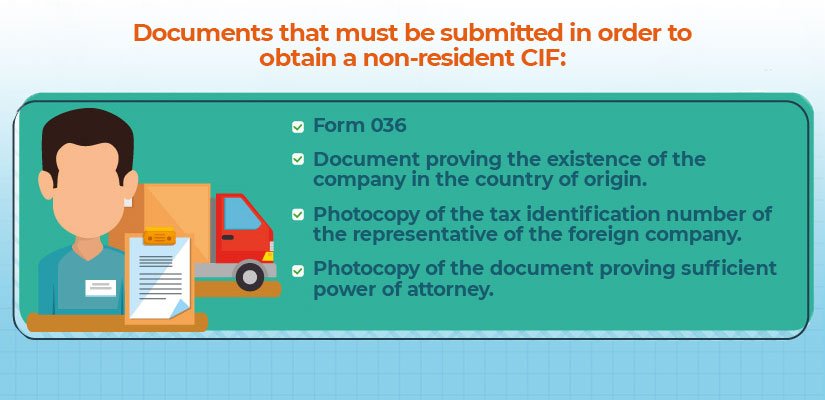

What documentation is necessary to apply for the NIF of foreign legal entities?

In the case of foreign entities wishing to apply for the NIF, in addition to the forms we have seen, the following documents must be provided:Document that accredits that the company in the country of origin exists.

Photocopy of the representative’s tax identification number.

Photocopy of the document accrediting sufficient power of attorney.

What steps must the foreign company follow in order to obtain a NIF?

The steps to obtain a non-resident NIF so that a foreign company can do business in Spain are simple:- Write a power of attorney in favor of LEIALTA. The power of attorney is a public document that is granted before a Notary and allows LEIALTA to act on behalf of the foreign company in order to obtain the CIF. For the power of attorney to be valid, it must:

- Be granted by the administrative body of the foreign company (board of directors, sole administrator or joint and several or joint administrators).

- Include all the necessary powers so that all the steps to obtain the non-resident CIF and the electronic certificate can be carried out.

- Appoint a LEIALTA lawyer as the fiscal representative of the company in Spain. The fiscal representative must have fiscal residence in Spain, which means that he/she must live in Spain for at least 183 days a year.

- Incorporate the following data: name of the company, address, identification of the person signing, position held and date of appointment, identification of the attorney-in-fact (in this case, a LEIALTA partner) and definition of the powers granted depending on the service requested.

- Obtain the document proving the existence of the company in the country of origin.

- Include in the documents the Hague Apostille and send them to LEIALTA’s offices in Spain.

- Have all the documents translated by an official translator.

- Present the form 036 together with the documentation and obtain the CIF number.

: rates, forms and tax rules for foreigners")

Hi, I´ve recently had my NIF revoked. I´m trying to recover it, How does this affect my paperwork? Best regards

Hi Samuel,

As you do not have the CIF operational, you cannot carry out procedures such as:

o Making entries in the public register.

o Refraining the notary from authorizing any public instrument relating to declarations of intent, legal acts involving consent, contracts, and legal transactions of any kind, as well as prohibiting access to any public registry, including those of an administrative nature, unless the tax identification number is reinstated.

o The registration certificates of the entity holding the revoked number will state that it has been withdrawn.

o Make debits and credits to accounts or deposits opened in credit institutions.

o Obtain a certificate stating that they are current with their tax obligations.

o Deregistration from the Register of Intra-Community Operators (ROI) and the Monthly Return Register (REDEME).

Best regards,

Paul

Hi, can a company with a revoked nif carry out activities? Best regards

Dear tom,

Logically, we must understand that yes. It would not make sense for the tax administration to require taxpayers to provide the documentation that proves the economic activity that the company will carry out to reinstate a revoked NIF, and on the other hand, it would not be allowed to continue carrying out economic activities.

However, with its revoked NIF, the company will encounter “operational problems” if it has to file self-assessments, returns, and documentation. It must also do so electronically, and if the NIF and the FNMT digital certificate are revoked, it will not be able to comply with all these formalities. Best regards

Hello, is there a deadline for applying for a NIF for non-residents? Do I have to obtain it before starting the procedure? Thanks!

Hi Justin, the time to apply for the NIF when setting up a company is within the month following the date of incorporation, but always before carrying out any transaction, starting any economic activity, or hiring personnel. For example, if you create a company on 1 April, you have until 1 May to complete this procedure.Best regards.

Hello, to carry out intra-community operations in my company, I must obtain a community NIF, how can I get it? Best

Hello James,

To obtain the Community VAT number you must apply for it using the census declaration 036/037 with a registration request. The assignment of the EU VAT number means that you will be included in the VIES census. The Tax Administration must resolve the application within three months, and if after these three months, you have not obtained it, this means that the application has been rejected.

It´s important to remember that obtaining the Community VAT number means that you are automatically included in the European VIES census and the Register of Intra-Community Operators, which is an essential requirement for the operation to be exempt from VAT.

Best regards

Hello,

I´m currently working in Germany, but I am moving to Spain soon, and my company has allowed me to continue teleworking for them. But they only have a NIF for non-residents in Spain (they don’t have a subsidiary or anything like that). Under these conditions, how could they register me in Spain? Best regards

Dear James,

With a non-resident VAT number, hiring a team member and complying with Social Security and quarterly withholding tax obligations is possible. It is the easiest and simplest structure for engaging a remote worker.

You have to present a 036 registration form and register for team member withholdings and, with the electronic certificate of said CIF register it with Social Security. Then you can finally write the employment contract with this body.

Best regards

Hello, Is it possible to have a bank account in Spain for an American LLC? Best regards

Dear Hailey

It is possible if you have a Spanish CIF from the LLC entity. You would have to arrange with the bank the documentation they will ask you for to open a bank account.

Best regards.

How are you? I have a CORP in Florida, how long would it take to start operating in Spain? Best regards

Dear Sophie, it can take about 15 days. Spain is a somewhat bureaucratic, so you must be well advised along the way. Best regards.

Hi, I have an LLC, but I want to have the warehouse or stock in Spain (my home) to save the cost of transport, etc., because most of my customers are from Spain and the EU. Is there any way to send orders from Spain having an LLC USA (to avoid the high cost of the fee of being self-employed)? Best regards

Dear Mike,

Perhaps you can obtain a non-resident CIF from the US LLC entity in Spain and operate in Spain this way. In this case, paying autonomous tax is unnecessary as you do not create a company in Spain.

You must be careful not to be considered a Permanent Establishment due to your activity and structure in Spain (stipulated in art 13 of the Non-Resident Income Tax). Best regards